INTRODUCTION

Companies are increasingly turning to demergers as a method of separating out various parts of a business. The decision to split off a trade or subsidiary from a company or group may be undertaken for a multitude of reasons including streamlining operations, ring-fencing liabilities, succession planning or shareholder disputes.

There are three broad routes to carrying out a demerger:

- The statutory route (an exempt demerger)

- Liquidation under the Insolvency Act 1986

- Reduction of capital (a Companies Act 2006 reconstruction)

This note focuses solely on the capital reduction route, covering the key tax implications and the principal qualifying requirements.

Parts 1 and 2 of this demerger series focus on demergers under the alternative routes of (1) a statutory demerger and (2) a liquidation reconstruction.

A capital reduction demerger is an alternative to a statutory demerger where the requirements of the latter cannot be met. In practice there are two main reasons why a statutory demerger is not possible, either because there are companies in the group that are not trading companies, or because the demerger is in anticipation of a sale of one or more of the companies involved in the demerger.

A capital reduction demerger is also seen as an alternative to a liquidation reconstruction where, for example, the shareholders do not wish to be associated with a company liquidation. It is often the natural choice where the company being demerged wishes to continue and has sufficient share capital to effect the capital reduction.

Capital reductions have been used more widely following the changes in Companies Act 2006, which removed the requirement to apply to the courts to enable a limited company to reduce its share capital.

BASIC STEPS

In order to outline the basic mechanics, assume a holding company with two subsidiaries, and there is one shareholder who is a UK resident individual. The shareholder wants to separate the two subsidiaries so that each is held independently of the other. The requirements for a statutory demerger are not met and the shareholders would rather not be involved with a liquidation.

There are some preliminary issues that need to be addressed before proceeding with the mechanics of the demerger, and these can be summarised as follows:

In order to effect a capital reduction demerger the company must have issued share capital of more than the value of the subsidiary being demerged from the group. If it does not, a new holding company will need to be placed above the existing holding company so that the required share capital can be created. The subsidiaries being demerged would then be hived up to the new holding company.

The directors of the holding company will need to sign a declaration of solvency as part of the capital reduction process, and there are criminal sanctions in relation to inaccurate or false declarations that they need to be fully aware of. There are other legal issues and requirements that need to be addressed in relation to a capital reduction demerger.

The basic steps to effect a capital reduction demerger would be as follows:

- The shareholder forms a new company (Newco) with a small number of subscriber shares.

- The holding company effects a capital reduction as follows:

- The demerged subsidiary is transferred to Newco;

- Newco issues new shares to the shareholder as consideration for the acquisition of the subsidiary, and in satisfaction of the capital reduction;

- The share capital of the holding company is reduced by an amount equal to the value of the demerged subsidiary.

- As a result of the demerger:

- The holding company is left with a reduced share capital and continues to hold the remaining subsidiaries;

- The shareholder will hold all the remaining share capital of the original holding company and of Newco, which holds all the issued share capital of the demerged subsidiary.

Although there are various taxes to consider in relation to these transactions, by effecting the demerger in accordance with the statutory provisions, no tax liabilities should arise in the above situation.

VARIATIONS ON THE DEMERGER STEPS

Innumerable variations on the basic demerger model are possible, so as to deal with specific situations. In every case the tax position would have to be considered to ensure that tax liabilities are mitigated as far as possible.

Where the holding company has a number of shareholders, they may want to separate subsidiaries into different ownership. This is referred to as a partition. It is still possible to avoid most of the potential tax charges apart from stamp duty, which would be payable at ½% on the value of the shares issued in each of the new companies as consideration for the companies they acquire.

There may not be a holding company, but instead the top company in the group carries on its own business. If the company has sufficient issued share capital that company can effect a demerger of one of its subsidiaries by way of a capital reduction. However, it may be necessary to put a new holding company over the existing top company by way of a share for share exchange, and then transfer some or all of its subsidiaries under the new holding company. The group would then be in a position to effect the capital reduction demerger.

Assets can be transferred between group companies in preparation for the demerger. This needs to be done with care to ensure that a corporation tax charge does not arise. Where land and buildings are transferred, there could also be an SDLT charge depending on how the transfers take place.

Whenever a capital reduction demerger is being considered it is vital that each of the steps is considered carefully to ensure that all potential tax issues are addressed. This is usually done by preparing a detailed steps plan, which also ensures that all parties understand what is involved and what documentation or agreements are required from the start.

CLEARANCE APPLICATION

A clearance application will be required to ensure that HMRC are satisfied that the demerger is being done for bona fide commercial reasons and not for the avoidance of tax. If HMRC do not give clearance and the demerger goes ahead, anti-avoidance provisions can be used by HMRC to counter what they see as a tax advantage. This could mean that on a share for share exchange a disposal of the old shares would be chargeable be capital gains tax rather than being rolled into the new shares, and in some circumstances proceeds arising from the demerger could be taxed as a dividend rather than under capital gains tax rules.

CONCLUSION

A capital reduction demerger is similar to a liquidation demerger, but is appropriate where the shareholders do not wish to disturb the wider group or are uncomfortable about being involved in a company liquidation. A capital reduction demerger is a useful alternative to a statutory demerger when the detailed requirements of the latter cannot be met. However, the steps must be considered carefully to ensure that there are no unexpected tax liabilities. It is usually possible to effect a capital reduction demerger with little or no tax liabilities arising.

The information contained in this document is for information only. It is not a substitute for taking professional advice. In no event will Dixon Wilson accept liability to any person for any decision made or action taken in reliance on information contained in this document or from any linked website.

This firm is not authorised under the Financial Services and Markets Act 2000 but we are able in certain circumstances to offer a limited range of investment services to clients because we are members of the Institute of Chartered Accountants in England and Wales. We can provide these investment services if they are an incidental part of the professional services we have been engaged to provide.

The services described in this document may include investment services of this kind.

Dixon Wilson

22 Chancery Lane

London

WC2A 1LS

T: +44 (0)20 7680 8100

F: +44 (0)20 7680 8101

DX: 51 LDE

www.dixonwilson.com

dw@dixonwilson.co.uk

Related articles

Demergers - The Statutory Route

Businesses use demergers as a method of separating out various parts of a business. The decision to split off a trade or subsidiary from a company or group may be undertaken for a multitude of reasons including streamlining operations, asset protection, succession planning or shareholder disputes.

There are three broad routes to carrying out a demerger:

- The statutory route (an exempt demerger)

- Liquidation under the Insolvency Act 1986

- Reduction of capital (a Companies Act 2006 reconstruction)

This note focuses solely on the statutory route. The principle manner the statutory route is undertaken is via a direct or indirect demerger, both of which are explored below.

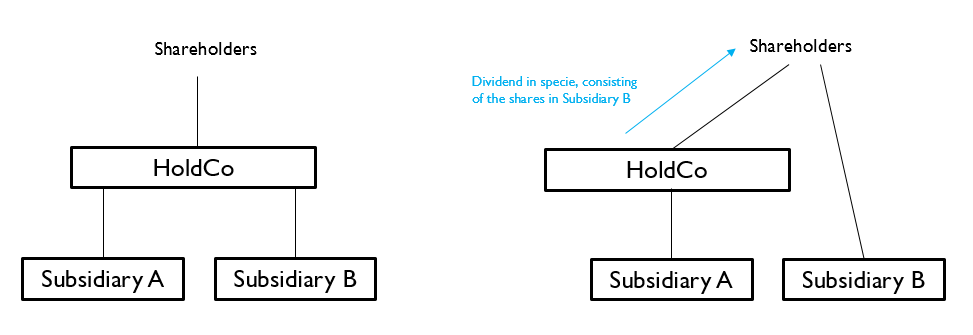

A direct demerger involves a distribution by a distributing company (HoldCo) of its shares in one of its wholly owned subsidiaries, the demerging company (Subsidiary B), to the distributing company’s shareholders (See Figure 1).

Figure 1 - Diagrams of direct demerger:

The key tax implications of a direct demerger are as follows:

- The distribution is exempt for income tax purposes in the hands of the shareholders.

- No capital gains tax arises to the shareholders as any gains are effectively rolled over.

- There is no stamp duty on the distribution in specie.

- The distributing company may have a chargeable gain on disposal but this would not be taxable if the substantial shareholding exemption applies.

- There would technically be degrouping charges in the demerging company for any assets held that had been transferred to it at no gain no loss within the last six years. However, if the distribution is exempt the degrouping charges are washed away.

- No VAT chargeable on the distribution.

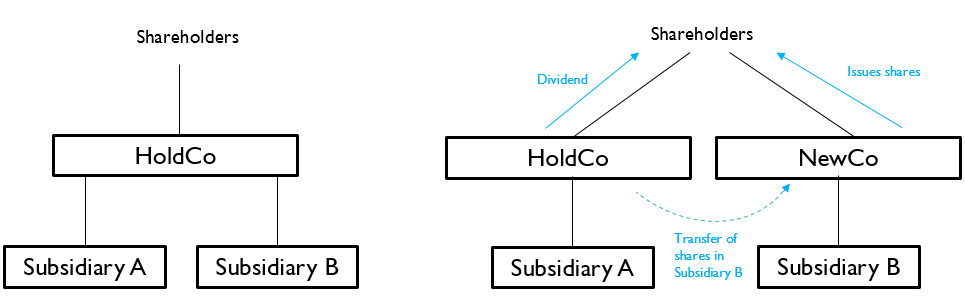

An indirect demerger involves either (a) the assets of a trade or (b) the shares in a company to be demerged (Subsidiary B) being transferred to a newly incorporated company (Newco). Newco in turn issues shares to the distributing company’s shareholders in satisfaction of the distribution by the distributing company (HoldCo) (See Figure 2).

Figure 2 - diagrams of indirect demerger:

The key tax implications of an indirect demerger are as follows:

- The distribution is exempt for income tax purposes in the hands of the shareholders.

- No capital gains tax arises to the shareholders as any gains are rolled over.

- There is no exit charge in the distributing company.

- No stamp duty on the basis that the demerger is across the board. Where the transfer is to certain members only, there will be a charge, although is ordinarily limited to 0.5 per cent.

- No VAT chargeable on the distribution.

There are a number of strict conditions that must be met for a direct or indirect demerger to fall within the provisions of the statutory route; including:-

- The companies must all be EU Member State resident.

- Both distributing and demerged companies must be trading companies, or in the case of the parent company, a member of a trading group.

- The demerged company must be a 75 per cent subsidiary.

- The distribution must be for the benefit of the trade.

- The distribution must not be made for the purposes of:

- the avoidance of tax or stamp duty

- the acquisition by persons who are not members of control of the company;

- the cessation of a trade or its sale;

Given the number and complexities of the qualifying requirements, advice should be sought from a tax professional on a case-by-case basis.

There is a need to consider potential future transactions, ordinarily within five years of the demerger, under the chargeable payments rules. These rules require that the distribution must not form part of a scheme or arrangement the main purpose, or one of the main purposes, of which is the making of a chargeable payment. The definition of “chargeable payment” is broad. It includes any payment, other than a qualifying distribution, by a company concerned with the exempt distribution to a member of the company or to a member any other company concerned in the distribution in respect of their shares which either is not made for genuine commercial reasons of forms part of a tax avoidance scheme.

These provisions stem from a concern that the relief under the statutory demerger provisions could be used to provide shareholders with a cash payment, or other assets, in a manner that allowed shareholder to escape income tax and the company to escape corporation tax.

It is common practice for advance clearance to be sought to confirm the exempt distribution status of a demerger and also separately to ensure payments would not be deemed chargeable payments.

Within 30 days of an exempt distribution or chargeable payment, a return must be filed with HM Revenue and Customs providing full details of the transaction.

The use of the statutory demerger route can prima facie seem like the most straightforward route for splitting up a trade or subsidiary from a company or group. Where the qualifying requirements are met there are significant income tax and corporation tax reliefs available.

That said, the qualifying requirements are quite onerous and there are several common scenarios that will not benefit from the statutory demerger legislation; including where an investment business is to be split from a trading business or where a business is to be separate so that it can be sold in the near future. In these situations it might be necessary to consider (1) a liquidation demerger or (2) a reduction in capital demerger.

Demergers - Liquidation Reconstruction under s 110 Insolvency Act 1986

Companies are increasingly turning to demergers as a method of separating out various parts of a business. The decision to split off a trade or subsidiary from a company or group may be undertaken for a multitude of reasons including streamlining operations, ring-fence liabilities, succession planning or shareholder disputes.

There are three broad routes to carrying out a demerger:

- The statutory route (an exempt demerger)

- Liquidation under the Insolvency Act 1986

- Reduction of capital (a Companies Act 2006 reconstruction)

This note focuses solely on the liquidation route, covering the key tax implications and the principal qualifying requirements.

Part 1 and Part 3 of this demerger series focus on demergers under the alternative routes of (1) a statutory demerger and (2) a reduction of capital demerger.

A liquidation demerger is an alternative to a statutory demerger where the requirements of the latter cannot be met. In practice there are two main reasons why a statutory demerger is not possible, either because there are companies in the group that are not trading companies, or because the demerger is in anticipation of a sale of one or more of the companies involved in the demerger.

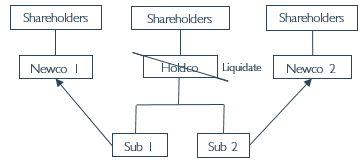

In order to outline the basic mechanics, assume a holding company with two subsidiaries, and there is one shareholder who is a UK resident individual. The shareholder wants to separate the two subsidiaries so that each is held independently of the other. The requirements for a statutory demerger are not met.

The basic steps to effect a liquidation demerger would be as follows:

- The shareholder forms two new companies with a small number of subscriber shares;

- The holding company appoints a liquidator who enters into a tripartite agreement with the shareholders and the two new companies in which it is agreed that the liquidator will distribute the shares in a subsidiary to each of the new companies, and those companies will issue new shares to the shareholder as consideration for the transfer of shares in the subsidiaries.

- Having distributed all the assets of the holding company in the course of the liquidation, the holding company is struck off the register at Companies House.

As a result, the shareholder holds all the share capital of two new holding companies, each of which holds all the shares in one of the subsidiaries.

Although there are various taxes to consider in relation to these transactions, by effecting the demerger in accordance with the statutory provisions, no tax liabilities should arise in the above situation.

Innumerable variations on the basic liquidation demerger model are possible, so as the deal with specific situations. In every case the tax position would have to be considered to ensure that tax liabilities are mitigated as far as possible.

Where the holding company has a number of shareholders, they may want to separate subsidiaries into different ownership. This is referred to as a partition. It is still possible to avoid most of the potential tax charges apart from stamp duty, which would be payable at ½% on the value of the shares issued in each of the new companies as consideration for the companies they acquire.

There may not be a holding company, but instead the top company in the group carries on its own business. This means that it may not be feasible to put that company into liquidation. One solution would be to put a new holding company over the existing top company by way of a share for share exchange, and then transfer some or all of its subsidiaries under the new holding company. The group would then be in a position to effect the liquidation demerger.

Assets can be transferred between group companies in preparation for the demerger. This needs to be done with care to ensure that a corporation tax charge does not arise. Where land and buildings are transferred, there could also be an SDLT charge depending on how the transfers take place.

Whenever a liquidation reconstruction is being considered it is vital that each of the steps is considered carefully to ensure that all potential tax issues are addressed. This is usually done by preparing a detailed steps plan, which also ensures that all parties understand what is involved and what documentation or agreements are required from the start.

A clearance application will be required to ensure that HMRC are satisfied that the demerger is being done for bona fide commercial reasons and not for the avoidance of tax. If they are not satisfied, the shareholders will be treated as having made a chargeable disposal of their shares in the holding company, based on the market value of the assets transferred by the liquidator to the new companies.

A liquidation demerger is a useful alternative to a statutory demerger when the detailed requirements of the latter cannot be met. However, the steps must be considered carefully to ensure that there are no unexpected tax liabilities. It is usually possible to effect a liquidation reconstruction with little or no tax liabilities arising.

However, sometimes the shareholders do not want to be involved in a liquidation because of commercial or reputational reasons, so alternatives need to be considered, such are a capital reduction demerger.