BACKGROUND

The worldwide debt cap rules were repealed effective from 1 April 2017 and have been replaced by the new corporate interest expense rules.

The motivation behind the new rules is to restrict the amount of tax relief for interest expenditure claimed by large or multinational groups that are highly leveraged.

For companies that have a year-end spanning this commencement date (e.g 31 December 2017) the results for the period will need to be split between pre and post 31 March 2017. This will usually be on a pro rata basis, unless this leads to an unfair result.

The new rules will apply to more groups and companies than the old worldwide debt cap rules, as the old rules did not apply where the shareholding of the ultimate parent company in the UK subsidiaries was less than 75%. The new rules will apply to all groups and also potentially to individual companies.

GROUP DEFINITION

For these purposes ‘group’ follows the accounting definition and so will consider the largest group for which consolidated accounts are prepared. The parent of this group is the ‘ultimate parent’. Where there is a change in ownership the group will change and any excess capacity (see below) would be lost.

EXEMPTIONS

The main exemptions (only one is required) to applying the rules are:

- Companies or groups where aggregated UK net interest expense does not exceed £2million. Where aggregated UK net interest expense (broadly interest payable less interest receivable for the UK companies of the group) is less than £2million, the rules will not need to be applied. Exchange gains and losses and impairment losses and reversals are not included in these calculations.

- Public benefit infrastructure. Where a company is involved with a public infrastructure project, certain income tests are met and where lending is not from a related party, an election for exemption can be made prior to the end of the accounting period and cannot be reversed for 5 years.

- Buildings that are part of a UK property business and let on a short-term basis. This exemption is designed mostly for student accommodation and joint ventures between property development companies and universities with specific criteria that needs to be met. An election is required prior to the end of the accounting period and cannot be reversed for 5 years.

- Funds accounting for subsidiary companies at fair value. Where portfolio companies are not consolidated for accounting purposes and are considered to be held separately.

LEGISLATION AND GUIDANCE

The Corporate Interest Restriction legislation in Part 10 Taxation (International and Other Provisions) Act (TIOPA) 2010 applies from 1 April 2017. Minor technical amendments to that legislation are included in the current Finance (No.2) Bill.

The rules are very complex covering hundreds of pages of legislation and 577 pages of HMRC guidance and so this update only covers the main concepts and not the full detail. Where these rules are relevant it is important to perform detailed calculations as there are a number of potential elections that can be made which can produce different results.

SUMMARY OF MAIN RULES

The principal of the new rules is that, where the exemptions are not available, groups and individual companies must consider whether the aggregate net interest expense for the UK companies within the group is too high by reference to:

i) The worldwide net interest expense (‘Modified debt cap’), (‘ANGIE’ if applying the fixed ratio rule and ‘QNGIE’ for group ratio rule).

ii) The ratio of net UK interest over UK tax EBITDA, not exceeding 30% (‘Fixed ratio rule’).

iii) The ratio of worldwide net interest expense (also known as ‘QNGIE’) over group EBITDA (‘Group ratio rule’). This third condition is optional and should only be considered if the fixed ratio for the second condition exceeds 30%. 100% is used where the group ratio exceeds 100% and 30% where the ratio is less than 30%.

NB: Conditions ii) and iii) are still subject to condition i), i.e. the allowable interest expense cannot exceed the modified debt cap.

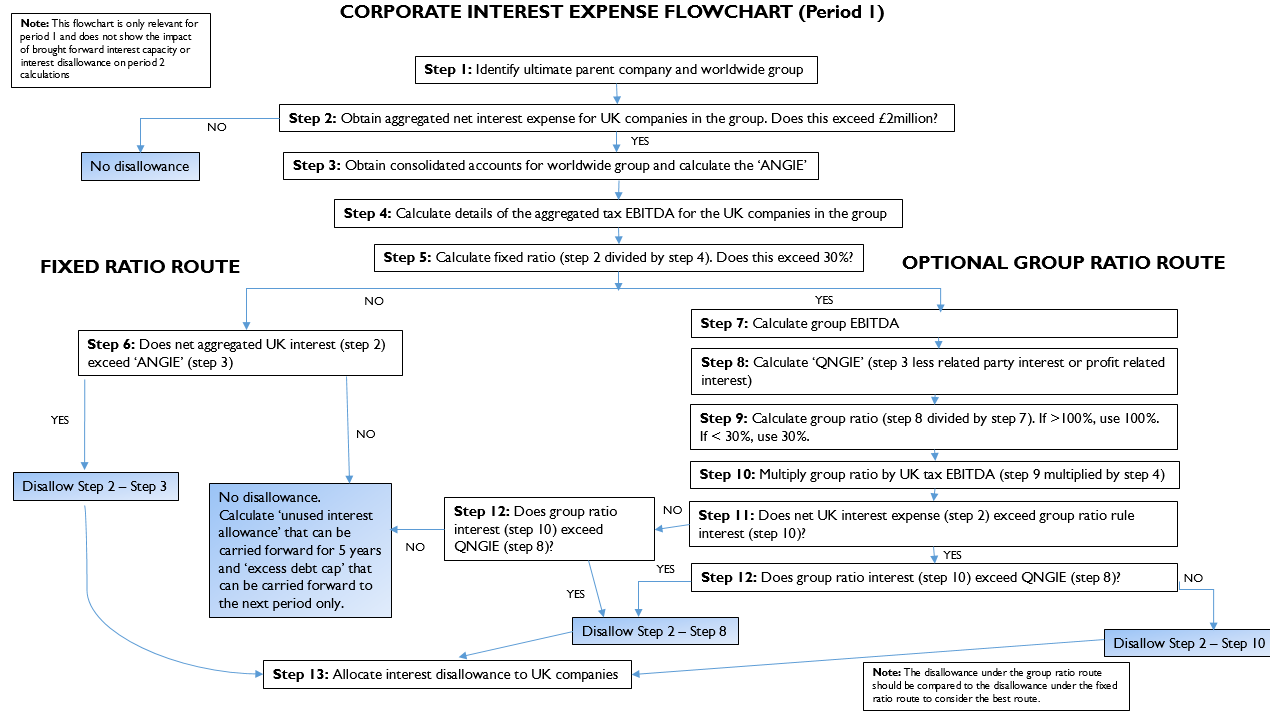

FLOWCHART

We have produced a flowchart to summarise the approach that should be taken in the appendix. It should be noted that this is a simplification of the main rules as it applies to year 1 and does not include the impact of excess brought forward interest capacity and excess debt cap which may be relevant after year 1.

Figure 1: Corporate Interest Expense Flowchart

NGIE, ANGIE and QNGIE

- NGIE is the Net Group Interest Expense per the consolidated group accounts (adjusted for exchange gains and losses and impairments).

- ANGIE (also ‘Modified debt cap’) is Adjusted NGIE. The most common adjustment is capitalised interest. This is the debt cap under the fixed ratio rule.

- QNGIE is Qualifying NGIE, which is ANGIE less related party interest or profit related interest. This is the debt cap under the group ratio rule.

- A number of elections are possible when calculating these figures.

EXAMPLE

Group A has net UK interest expense of £5m, UK tax EBITDA of £10m, group NGIE of £2m, group capitalised interest of £2m, group related party interest of £0.5m and group EBITDA of £6m. What is the interest disallowable?

- ‘ANGIE’ is £4m (‘NGIE’ plus capitalised interest).

- ‘QNGIE’ is £3.5m (‘ANGIE’ less related party interest).

- The ‘fixed ratio’ is 50% (net UK interest/ UK tax EBITDA) = £5m/£10m. Condition ii) restricts the fixed ratio to 30%, so the interest allowed under this rule would be £3m (£10m x 30%).

- Under conditions i) and ii) the interest deduction permitted is the lower of the fixed ratio amount and ‘ANGIE’ i.e. £4m. Therefore £2m interest is disallowable (£5m - £3m).

- However, it is possible to elect to apply the group ratio. The group ratio is calculated as (QNGIE/group EBITDA) = 58% (£3.5m /£6m). This is applied to the UK tax EBITDA which results in potential interest allowance of £5.8m (58% x £10m). However, there is the ultimate cap of QNGIE of £3.5m.

- Therefore, the disallowed amount is £1.5m (£5m - £3.5m) and so the group ratio election is worthwhile as only £1.5m of interest is disallowable using the group ratio, whereas £2m would be disallowable using the fixed ratio.

ALLOCATION OF THE DISALLOWED AMOUNT AND CARRY FORWARD OF DISALLOWED AMOUNT

HMRC’s default approach is that any disallowed amount will be allocated to UK group members on a pro-rata basis.

A reporting company can be nominated to allocate the disallowed amount on an alternative basis, in any way the group decides is appropriate. The only restriction is that the allocated disallowance cannot exceed an individual company’s net interest expense.

The deadline for nominating the reporting company is 6 months after the year-end (see more details below), however the actual interest return showing the disallowed amounts is not required to be filed until 12 months after the year-end.

The disallowed amount is carried forward in the company that it has been allocated to and is added to interest of the following year for the purposes of the following year’s calculations.

Where the group companies do not consent to the group allocation, HMRC have the power to allocate the disallowance on a pro-rata basis.

INTEREST CAPACITY, UNUSED INTEREST ALLOWANCE AND EXCESS DEBT CAP

A group’s ‘interest capacity’ is the aggregate of the interest allowance for the period and any unused interest allowance brought forward from an earlier period.

Where there is ‘unused interest allowance’, this can be carried forward on a group basis for up to 5 years, to be utilised in future years. This will arise where the fixed ratio interest, or group ratio interest (where a group ratio election is made), exceeds the net UK interest for the group.

However if the ultimate parent changes then any excess capacity or unused interest allowance will be lost.

The ‘excess debt cap’ applies in limited situations where usually a disallowance arises due to the modified debt cap (‘ANGIE’ or ‘QNGIE’), but in that particular period the fixed ratio or the group ratio is the limiting factor. The excess debt cap is calculated as (ANGIE - 30% x UK tax EBITDA) if the fixed ratio rule is used or (QNGIE - group ratio % x UK tax EBITDA) where there has been an election to use the group ratio. This can be carried forward just to the next period and increases the ANGIE for that period, where the modified debt cap (‘ANGIE’) is the limiting factor of the next period.

INTEREST

The rules contain a lot of detail on what should and shouldn’t be included in the definition of interest. This is unfortunately not simply the case of taking the figures from the finance income and cost note of the accounts for the group figures or from the tax returns for the UK interest figures. This is because certain items on the balance sheet will need to be included (e.g capitalised interest) and certain items in the finance income and costs notes will need to be excluded (e.g exchange gains and losses and impairment losses and reversals). There are also a number of elections available in relation to movements on derivatives.

TAX EBITDA

This needs to be calculated from each company’s corporation tax return, adjusted to remove interest, amortisation, capital allowances and group relief. There is an option to exclude fair value movements on derivatives. This works in a similar manner to the Disregard Regulations.

ADMINISTRATION

MECHANICS OF THE RETURN

The corporate interest restriction (“CIR”) return is separate to a company’s corporation tax return. The deadline for filing the CIR return is 12 months after the end of the relevant accounting period.

There are two types of return, an abbreviated return and a full return. It is also possible to file no return, where there is no disallowance in the period and HMRC have not appointed a reporting company. However, not submitting a return may lead to missed elections and allowances in later years.

APPOINTING A REPORTING COMPANY

Each group is required to appoint a reporting company to HMRC within 6 months of the year-end. E.g. for a 31 March 2018 year-end this should be completed by 30 September 2018. The appointment of a reporting company can be revoked.

Alternatively, HMRC can nominate a reporting company within 3 years of the year-end. Guidance suggests that HMRC will do this if there is any disallowance under the rules.

The reporting company must notify the eligible companies that it has been appointed. It will be granted statutory powers to require the relevant data to complete a CIR return from other UK group companies.

ABBREVIATED RETURN

An abbreviated return can only be used where there are no disallowances or activations and the group does not wish to carry forward unused interest allowances. It is useful if the group wishes to make elections, which cannot be made if no return is submitted.

A group can choose to file an abbreviated return initially and a full return at a later date (within the amendment window) if they wish to do so.

FULL RETURN

Where there are interest disallowances or where the group wishes to carry forward interest allowances, the reporting company is required to file a full interest restriction return to HMRC within 12 months of the end of the relevant accounting period. The return can be amended up to 36 months after the end of the accounting period. The normal time limit for HMRC opening an enquiry is 39 months.

The return will contain details of the group’s net UK interest expense, its interest capacity and the allocation of any interest which is restricted under the rules between UK members of the group.

If a UK member does not agree with the allocation in the return, it can elect to be a non-consenting company, in which case its interest costs will be restricted by an amount equal to its pro rata share of the restricted interest costs of the group, calculated by reference to the proportion that its net interest expenses to total net interest expenses of all UK members of the group with a net interest expense.

SUMMARY

The new rules are complex and will require detailed calculations where the £2million net UK interest de minimus threshold is exceeded by the UK members of a group.

It is recommended that the expected impact on the group in the current year and future years is modelled as soon as possible so the best approach can be considered, in particular for any elections that may be available.

Groups that could potentially be affected by the new rules, either in the current period or in the future, should consider appointing a reporting company within 6 months of the first accounting year-end after 1 April 2017.

The information contained in this document is for information only. It is not a substitute for taking professional advice. In no event will Dixon Wilson accept liability to any person for any decision made or action taken in reliance on information contained in this document or from any linked website.

This firm is not authorised under the Financial Services and Markets Act 2000 but we are able in certain circumstances to offer a limited range of investment services to clients because we are members of the Institute of Chartered Accountants in England and Wales. We can provide these investment services if they are an incidental part of the professional services we have been engaged to provide.

The services described in this document may include investment services of this kind.

Dixon Wilson

22 Chancery Lane

London

WC2A 1LS

T: +44 (0)20 7680 8100

F: +44 (0)20 7680 8101

DX: 51 LDE

www.dixonwilson.com

dw@dixonwilson.co.uk