INTRODUCTION

Businesses use demergers as a method of separating out various parts of a business. The decision to split off a trade or subsidiary from a company or group may be undertaken for a multitude of reasons including streamlining operations, asset protection, succession planning or shareholder disputes.

There are three broad routes to carrying out a demerger:

- The statutory route (an exempt demerger)

- Liquidation under the Insolvency Act 1986

- Reduction of capital (a Companies Act 2006 reconstruction)

This note focuses solely on the statutory route. The principle manner the statutory route is undertaken is via a direct or indirect demerger, both of which are explored below.

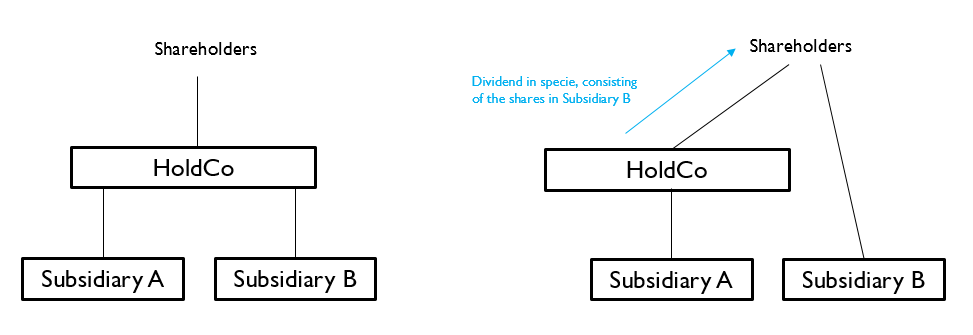

Direct Demerger

A direct demerger involves a distribution by a distributing company (HoldCo) of its shares in one of its wholly owned subsidiaries, the demerging company (Subsidiary B), to the distributing company’s shareholders (See Figure 1).

Figure 1 - Diagrams of direct demerger:

The key tax implications of a direct demerger are as follows:

- The distribution is exempt for income tax purposes in the hands of the shareholders.

- No capital gains tax arises to the shareholders as any gains are effectively rolled over.

- There is no stamp duty on the distribution in specie.

- The distributing company may have a chargeable gain on disposal but this would not be taxable if the substantial shareholding exemption applies.

- There would technically be degrouping charges in the demerging company for any assets held that had been transferred to it at no gain no loss within the last six years. However, if the distribution is exempt the degrouping charges are washed away.

- No VAT chargeable on the distribution.

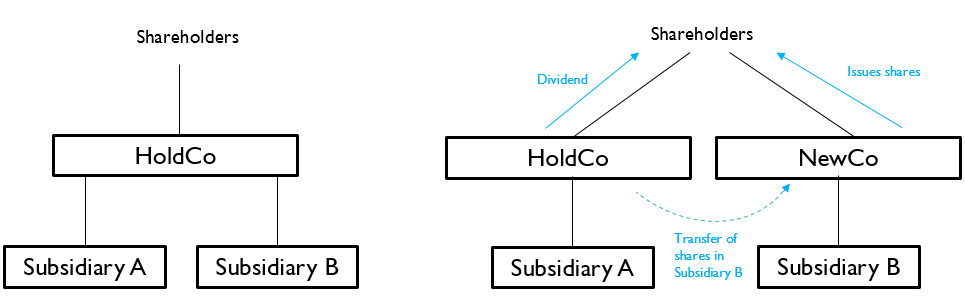

Indirect Demerger

An indirect demerger involves either (a) the assets of a trade or (b) the shares in a company to be demerged (Subsidiary B) being transferred to a newly incorporated company (Newco). Newco in turn issues shares to the distributing company’s shareholders in satisfaction of the distribution by the distributing company (HoldCo) (See Figure 2).

Figure 2 - diagrams of indirect demerger:

The key tax implications of an indirect demerger are as follows:

- The distribution is exempt for income tax purposes in the hands of the shareholders.

- No capital gains tax arises to the shareholders as any gains are rolled over.

- There is no exit charge in the distributing company.

- No stamp duty on the basis that the demerger is across the board. Where the transfer is to certain members only, there will be a charge, although is ordinarily limited to 0.5 per cent.

- No VAT chargeable on the distribution.

Principle Qualifying Requirements

There are a number of strict conditions that must be met for a direct or indirect demerger to fall within the provisions of the statutory route; including:-

- The companies must all be EU Member State resident.

- Both distributing and demerged companies must be trading companies, or in the case of the parent company, a member of a trading group.

- The demerged company must be a 75 per cent subsidiary.

- The distribution must be for the benefit of the trade.

- The distribution must not be made for the purposes of:

- the avoidance of tax or stamp duty

- the acquisition by persons who are not members of control of the company;

- the cessation of a trade or its sale;

Given the number and complexities of the qualifying requirements, advice should be sought from a tax professional on a case-by-case basis.

Chargeable Payments

There is a need to consider potential future transactions, ordinarily within five years of the demerger, under the chargeable payments rules. These rules require that the distribution must not form part of a scheme or arrangement the main purpose, or one of the main purposes, of which is the making of a chargeable payment. The definition of “chargeable payment” is broad. It includes any payment, other than a qualifying distribution, by a company concerned with the exempt distribution to a member of the company or to a member any other company concerned in the distribution in respect of their shares which either is not made for genuine commercial reasons of forms part of a tax avoidance scheme.

These provisions stem from a concern that the relief under the statutory demerger provisions could be used to provide shareholders with a cash payment, or other assets, in a manner that allowed shareholder to escape income tax and the company to escape corporation tax.

Advance Tax Clearance and Returns

It is common practice for advance clearance to be sought to confirm the exempt distribution status of a demerger and also separately to ensure payments would not be deemed chargeable payments.

Within 30 days of an exempt distribution or chargeable payment, a return must be filed with HM Revenue and Customs providing full details of the transaction.

Conclusion

The use of the statutory demerger route can prima facie seem like the most straightforward route for splitting up a trade or subsidiary from a company or group. Where the qualifying requirements are met there are significant income tax and corporation tax reliefs available.

That said, the qualifying requirements are quite onerous and there are several common scenarios that will not benefit from the statutory demerger legislation; including where an investment business is to be split from a trading business or where a business is to be separate so that it can be sold in the near future. In these situations it might be necessary to consider (1) a liquidation demerger or (2) a reduction in capital demerger.

The information contained in this document is for information only. It is not a substitute for taking professional advice. In no event will Dixon Wilson accept liability to any person for any decision made or action taken in reliance on information contained in this document or from any linked website.

This firm is not authorised under the Financial Services and Markets Act 2000 but we are able in certain circumstances to offer a limited range of investment services to clients because we are members of the Institute of Chartered Accountants in England and Wales. We can provide these investment services if they are an incidental part of the professional services we have been engaged to provide.

The services described in this document may include investment services of this kind.

Dixon Wilson

22 Chancery Lane

London

WC2A 1LS

T: +44 (0)20 7680 8100

F: +44 (0)20 7680 8101

DX: 51 LDE

www.dixonwilson.com

dw@dixonwilson.co.uk