INTRODUCTION

This note provides a brief summary of the PSC rules contained in the Small Business, Enterprise and Employment Act 2015.

From 6 April 2016 unlisted UK companies, LLPs and Societates Europaeae will have to create and keep up to date an additional statutory register with details about its Persons with Significant Control (‘PSCs’). From 30 June 2016 specified information about PSCs will also have to be provided when incorporating a company or LLP and when providing their annual confirmation statements (previously annual returns). The information will be publicly available. Further guidance on these aspects is awaited.

WHO IS A PSC?

A PSC is an individual who meets one or more of the following five conditions:

- the individual holds more than 25% of the company’s shares (whether directly or indirectly);

- the individual holds more than 25% of the voting rights in the company (whether directly or indirectly);

- the individual holds the right, directly or indirectly, to appoint or remove the majority of the company’s board;

- the individual has the right to, or does, exercise significant influence or control over the company; or

- the individual has the right to, or does, exercise significant influence or control over the activities of a trust where the trustees would meet any of the above four conditions in relation to the company if they were an individual (see the paragraph below on application to trusts for more information).

There is statutory guidance on the meaning of significant influence or control over companies which provides non-exhaustive principles and examples to aid interpretation of the fourth condition above. This should be consulted when identifying potential PSCs.

The guidance says that influence and control are alternatives. Where a person can direct the activities of the company that is indicative of ‘control’ and where a person can ensure the company generally adopts the activities they desire that is indicative of ‘influence’. A series of specific examples is given in the guidance of the sort of scenarios that might give rise to a person having the right to or actually exercising significant influence or control over a company. For example, a person would exercise significant influence or control if they are significantly involved in the management and direction of the company, such as a shadow director or someone else who regularly influences the board’s decision making.

In order to create the PSC register, all PSCs or companies that would be a PSC if they were an individual must be identified. This might be very straightforward, for example a standalone company with a sole director and shareholder. For a group of companies, or where there is a complex ownership structure, the task can be more complicated and we suggest the following process:

- Review each UK company’s register of members to identify shareholdings over 25%.

- Do the same looking for voting rights over 25%.

- Review the articles of association to see if anyone has the right to appoint or remove a majority of the board of directors.

- Where an individual does not meet one of the first three conditions but might be exercising significant influence or control over the company consider if the individual is otherwise a PSC by reference to the statutory guidance.

- Consider if any individuals exerting significant influence or control over a trust need to be treated as a PSC.

- Write to all those believed to be a PSC and seek confirmation of PSC status and relevant details.

- Create a draft PSC register – once 6 April 2016 is reached the register cannot be blank but must at least show what stage in the process of creating the PSC register has been reached.

- Update the PSC register as information is provided.

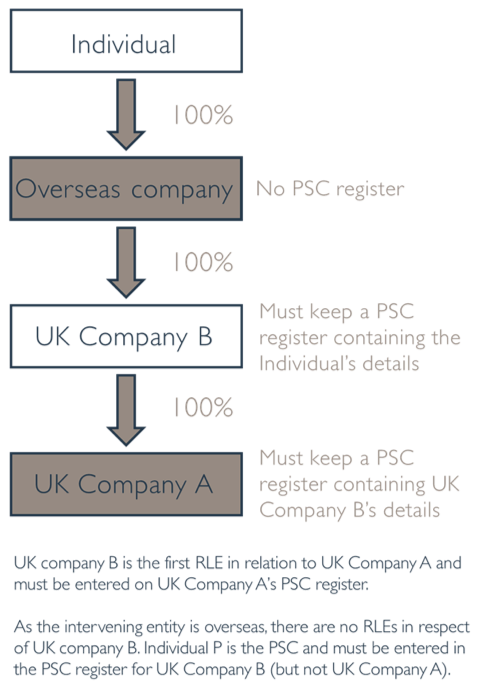

Although under the legislation a PSC has to be an individual, in some cases the name of a company will need to be entered in your PSC register. Starting at the bottom of the ownership chain you need to work upwards to find the first ‘relevant legal entity’ (RLE). Broadly speaking an RLE is a UK company which would have been a PSC if it were an individual. The first such RLE in the ownership chain is a “registrable RLE” and must be entered on the PSC register.

Example

WHAT INFORMATION TO INCLUDE IN THE PSC REGISTER

The following information about each PSC must be recorded in the register:

- Name

- Residential address (This will not be disclosed on the register. Where there is a serious risk of violence or intimidation, additional protection from disclosure to credit reference agencies and others can be applied for in the same way as already afforded to directors.)

- Service address

- Date of birth

- Particulars of significant control over the company

APPLICATION TO TRUSTS

Where a trust meets any of conditions one to four under Who is a PSC? above, we expect that the all the trustees will need to be included on the PSC register where they are individuals.

Also, under condition five, the details of any individual with significant influence or control over the activities of a trust which would be a PSC of a company if it were an individual should be entered on the PSC register of that company. Similarly, if a registrable RLE controls the trust it must be entered on the PSC register. The register should show the nature of trustees’ control i.e. each of the conditions one to four that are met.

Statutory guidance explains that a person has the right to exercise “significant influence or control” over a trust if that person has the right to direct or influence the running of the trust’s activities, such as:

- A right to appoint or remove any of the trustees, except through application to the courts or as a result of a breach of fiduciary duty by the trustees;

- A right to direct the distribution of funds or assets;

- A right to direct investment decisions of the trust;

- A right to amend the trust or partnership deed; or

- A right to revoke the trust.

In terms of actually exercising influence or control, this is likely to be found where a person is regularly involved in the running of the trust, for example because they issue instructions to the trustees which are generally followed.

Conclusion

It is not long until the new rules apply and directors and company secretaries should be taking steps to make sure they know who their PSCs and RLEs are and that their PSC registers are in an appropriate state of progress by 6 April 2016.

The information contained in this document is for information only. It is not a substitute for taking professional advice. In no event will Dixon Wilson accept liability to any person for any decision made or action taken in reliance on information contained in this document or from any linked website.

This firm is not authorised under the Financial Services and Markets Act 2000 but we are able in certain circumstances to offer a limited range of investment services to clients because we are members of the Institute of Chartered Accountants in England and Wales. We can provide these investment services if they are an incidental part of the professional services we have been engaged to provide.

The services described in this document may include investment services of this kind.

Dixon Wilson

22 Chancery Lane

London

WC2A 1LS

T: +44 (0)20 7680 8100

F: +44 (0)20 7680 8101

DX: 51 LDE

www.dixonwilson.co.uk

dw@dixonwilson.co.uk