Conversion To CIO

Recent legislation passed by parliament will allow charitable companies and community interest companies to convert to charitable incorporated organisations (CIOs).

CIOs were introduced by the Charities Act 2011. They offer the advantages of incorporation without the need to comply with Companies House requirements. Until recently only new or unincorporated charities could convert to a CIO.

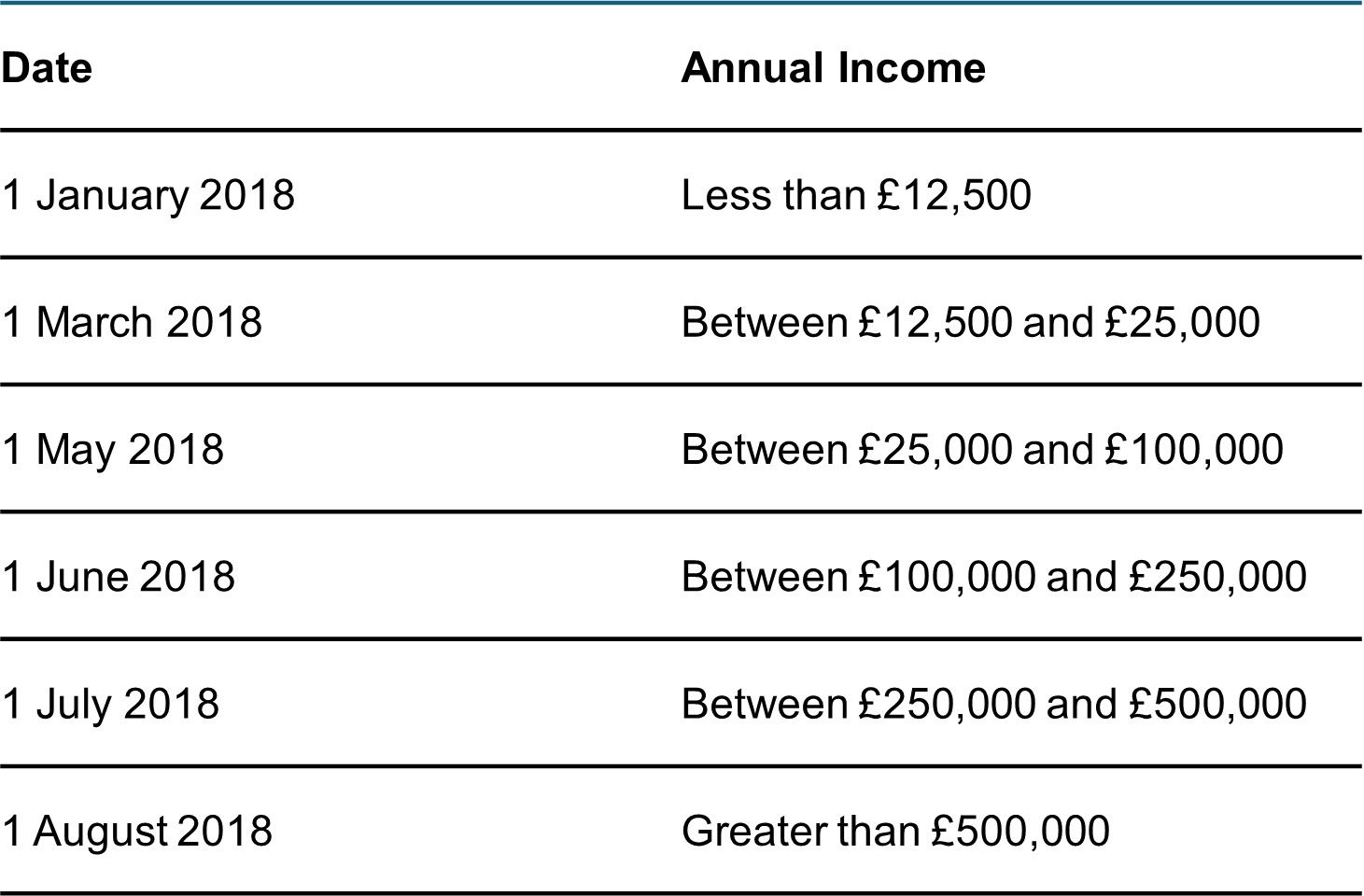

Charitable companies will be able to convert to CIOs from 1 January 2018 with a phased implementation timetable based on the organisation’s annual income. The dates and size limits are as follows:

As part of the new conversion process, before submission to the Commission, a new CIO constitution must be drafted, and a special resolution to convert must be made.

Budget - Changes To The Gift Aid Donor Rules

In his Autumn Budget, Chancellor Phillip Hammond announced several changes to the Gift Aid rules.

Current System

There are currently three thresholds governing the level of benefit donors (or persons connected with the donors) can receive from charities before their donations are no longer eligible for tax relief.

Currently a charity may provide:

- Benefits up to the value of 25% of donations up to and including £100.

- Benefits up to the value of £25 on donations between £101 and £1,000.

- Benefits of 5% (up to a maximum of £2,500) of donations over £1,001.

Changes

The middle threshold detailed above has now been scrapped, and so going forward:

- For donations up to £100, benefits up to the value of 25% may be provided.

- For donations over £100, benefits of 25% of the first £100, plus 5% of any additional amounts, may be provided (up to a maximum of £2,500).

In addition, the Chancellor announced that existing extra-statutory concessions surrounding the admission to a charity’s property, provision of literature, lifetime benefits, etc, will be legislated.

These changes are due to come into effect from April 2019.

Register Of Beneficial Ownership Of Trusts

As of 26 June 2017 there has been a legal requirement for HMRC to maintain a centralised register of trusts and complex estates.

For Charitable Trusts, the trustees will need to register the trust with HMRC once they have a tax liability arising from one of the following relevant taxes:

- Income tax

- Capital gains tax

- Inheritance tax

- Stamp duty land tax

- Stamp duty reserve tax

- Land and buildings transaction tax (Scotland)

The registration deadline of 31 January 2018 applies in respect of the tax year 2016-17. If the first taxable event occurs in subsequent years then the registration must be completed no later than 31 January after the end of that tax year.

For further information, please see the technical update relating to the Register of Beneficial Ownership of Trusts.

It is noted that the Charitable Trust is required to keep and maintain accurate and up-to-date written records of all the actual and potential beneficial owners of a trust, even if they do not need to report to HMRC.

For these purposes, a “beneficial owner” would include, amongst others, the Trustees and anyone with the power to appoint or remove Trustees.

General Data Protection Regulations

New General Data Protection Regulations (GDPR) are being introduced in the UK and the EU effective from 25 May 2018. The new rules will replace the existing Data Protection Act (DPA) and will affect all entities holding and processing personal data. There is no exemption available for charities.

In particular, there are specific rules for consent over direct marketing communications, and these include fundraising communications. Charities must now provide an “opt in” so that individuals can control how a charity communicates with them over the telephone, by post and by email.

The GDPR does not just apply to fundraising activities.

It is important that charities consider the personal data held for donors, volunteers, employees, beneficiaries and other individuals in accordance with GDPR.

See our technical update on GDPR for further details.

Additional key points include:

1. Reviewing how you obtain an individual’s consent to use personal data. You will need to explain clearly why you are collecting this data and how you intend to use it. Explicit consent is required to pass information on to third parties.

2. If an individual is registered with the Telephone Preference Service (TPS) then the charity will require specific consent in order to telephone that individual. If an individual is not registered, then the charity must be able to show that the individual has a legitimate interest in order to contact them, and cease doing so if the individual opts out.

3. Consent must be freely given, specific, informed and an unambiguous indication through a statement or clear affirmative action, such as actively ticking a box.

Volunteers are not treated differently to employees and should be trained on how to protect personal data.

The information contained in this document is for information only. It is not a substitute for taking professional advice. In no event will Dixon Wilson accept liability to any person for any decision made or action taken in reliance on information contained in this document or from any linked website. This firm is not authorised under the Financial Services and Markets Act 2000 but we are able in certain circumstances to offer a limited range of investment services to clients because we are members of the Institute of Chartered Accountants in England and Wales. We can provide these investment services if they are an incidental part of the professional services we have been engaged to provide. The services described in this document may include investment services of this kind.